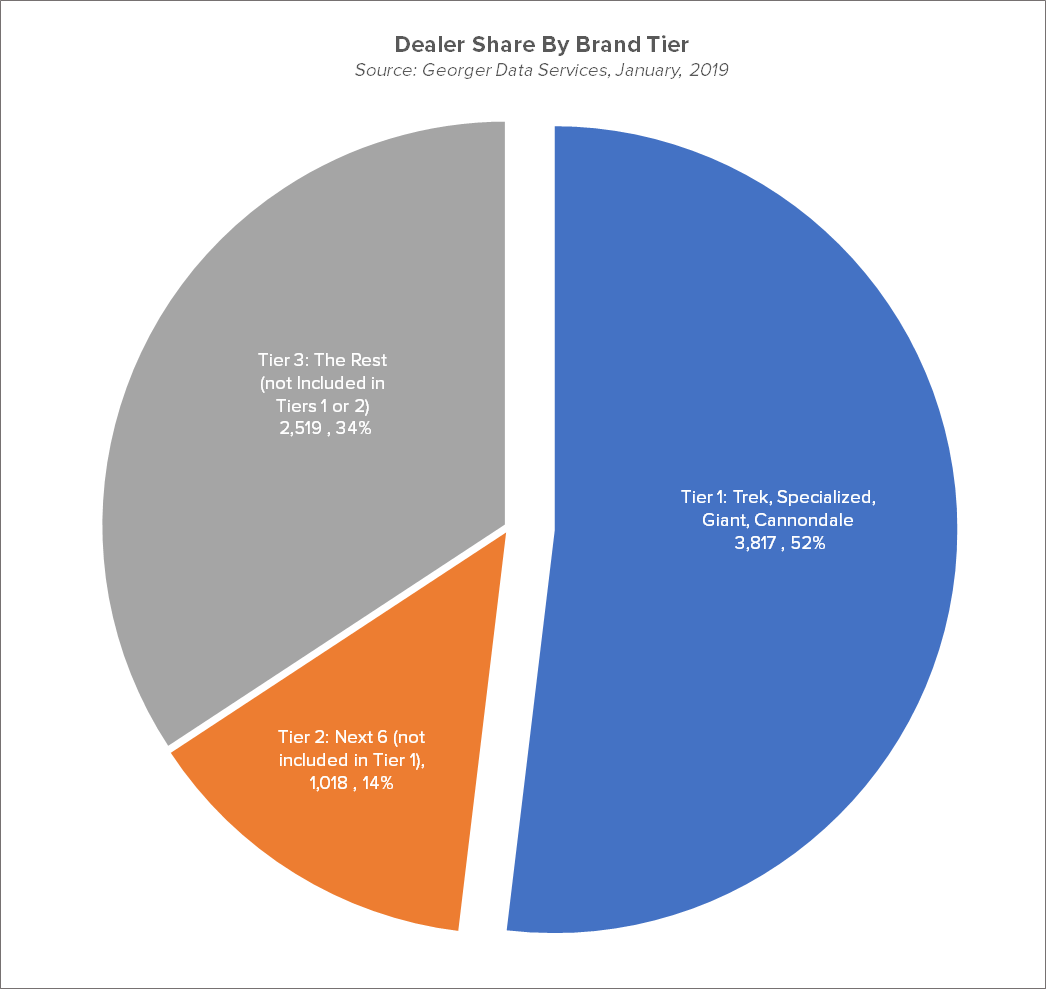

As we discussed in Part One, companies like Trek (17% of US dealers) and Specialized (16%) can be reasonably described as brand leaders in both bikes and many equipment categories. Others have pointed out those brands' share of sales is far greater than their share of storefronts. But the point is, you can't dominate a market with products that two-thirds of retail locations don't — and in fact, can't — sell.

To further muddy the water, marketing boffins are all over the map as to what constitutes a dominant share of market. Sources I checked peg that number anywhere between 25% (which either Trek or Specialized might reasonably be supposed to have) and 60% (which they almost certainly do not) of total sales. Like pornography, nobody seems to be able to define what a dominant share of market is, exactly, but everybody seems to know it when they see it.

Fortunately, there's a legal definition for purposes of trade law — in the EU, anyway. They define market dominance as a position of economic strength enjoyed by an undertaking which enables it to prevent effective competition being maintained on the relevant market by affording it the power to behave to an appreciable extent independently of its competitors, customers and ultimately of its consumers.

Like pornography, nobody seems to be able to define what a dominant share of market is, exactly, but everybody seems to know it when they see it.

Do any of our bike brands meet that test? I think not.

But there's another way to look at the dominance notion, what's called the four-firm concentration ratio, which is a fancypants marketing term for the combined market share of the top four brands in an industry. In US car manufacturers (as opposed to individual brands), it's General Motors, Ford, Toyota and Fiat Chrysler. Among running shoe brands in the US, it's Nike, Adidas, Under Armor, Skechers. You get the idea.

And of course, there are other measures. (Much) more about these concepts is available in this excellent Wikipedia article.

The top four U.S. bike brands — Trek, Specialized, Giant and Cannondale, in that order — are collectively represented in 52% of retail storefronts. In terms of sales, that share is undoubtedly much higher. (We can discuss why we don't have better sales numbers another time; let me know in the comments section if you're interested.) Taken collectively, the four brands have dominant market position, but because they don't behave collectively (which would invoke antitrust issues), they're not what we might label a quadropoly. Instead, let me propose Quadrumvirate as a term of convenience. Besides, Gang Of Four was already taken.

Enter The Big Blue Dragon

Now let's compare and contrast those leading bike brands' success with a truly dominant market force. In 2016, Credit Suisse Equity Research estimated Shimano's overall share of the global bicycle market at 70 – 80%. That's for all bikes, across all sales channels and price points, in the entire world.

Now that's a dominant market position.

Here in the U.S., Shimano's presence among U.S. retailers is functionally 100% ... despite the fact that it is effectively impossible for mainstream American bike shops to make a sustainable profit selling its aftermarket products.

Famously (and enforcement efforts with respect to Chain Reaction and related online vendors that went into effect earlier this month notwithstanding), retailers tell me Shimano groups and other high-dollar products are still consistently available direct to U.S. consumers via offshore internet companies .. near, at or even below the prices Shimano's own stateside distributors charge bike shops for the same equipment at wholesale.

The combined effect of low-cost Shimano product with perfect information via internet sales is huge. It's gutted a major revenue/profit stream for traditional bike dealers, permanently altered the U.S. specialty retail landscape, sent tens of millions of U.S. consumer dollars overseas .. and is effectively crushing Shimano's competitors in high-end markets worldwide.

The technical term for this is price leadership: the dominant brand sets a price and the rest of the market responds. If the dominant brand sets its prices higher than the rest of the market, its competitors can either raise their own prices, or keep them lower to emphasize their relative value proposition. If the dominant brand lowers prices, typically the rest of the market has to follow. What's interesting about the current situation is that the dominant brand gets to have it both ways — a premium-price reputation, yet available at huge discount to savvy shoppers. Which, in an era of perfect information, is everyone.

As I've often said, none of this is either good or bad. It is simply the way things are. Nor is the question of motive really relevant: industry speculation as to whether Shimano is A) at the mercy of international trade laws, as it claims, or B) passively encouraging transshipment (gray marketing) of its products from developing countries, OE customers and other sources into First World markets is neither here nor there.

Compounding the situation is the fact that there is no equivalent to the U.S. MAP trade law in either the EU or most other countries worldwide. But the bottom-line fact is the situation exists and continues to exist, despite Shimano's countermeasures. As a senior industry exec who asked not to be named puts it, "Shimano's position is that it needs to satisfy the customers needs regardless of where or how they buy its products."

Whatever it is, it's entirely consistent both with market behaviors in general and with predicted effects of Bike 3.0 specifically.

Endgame: dominant vs optimal market share

As cleverly foreshadowed near the top of the page, there is a critical difference between a dominant market share and an optimal one.

Regardless of actual size, a dominant market share is one with (paraphrasing now) the power to behave independently of its competitors, customers and ultimately of its consumers. Clearly, Shimano is a dominant brand in the U.S. and worldwide bike scene and has a dominant share of market, in every market where it does business. It can — and effectively does — tell the entire market what to do.

Optimal share, on the other hand, is rather different. The Harvard Business Review defines it this way: A company has attained its optimal market share in a given product/market when a departure in either direction from the share would alter the company's long-run profitability or risk (or both) in an unsatisfactory way. And that's where the Quadrumvirate currently resides.

In an essentially declining market (which, in constant dollars, ours has been for decades), there are a limited number of ways a brands can increase profits:

- It can increase the size of the overall customer base, or, as a former U.S. president put it, "make the pie higher." As I've mentioned elsewhere, this is an expensive proposition, and one which the powers that be and even industry organizations seem to have no appetite for. Generally, this role falls to the category leader, but absent a single dominant bike brand, it really requires a group effort. Why, yes, I am looking at you, Org Formerly Known As BPSA.

- It can add new products to its line, either by entering new categories or creating new niches within existing ones. To be sure, this is happening and continues to happen, but it's an incremental growth at best in a category as mature as ours.

- It can increase its retail footprint, which is a fancy way of saying "add more dealers." But given the way power is balanced in the supply chain, that's likely to be a disastrous move.

- It can bypass the supply chain, end-running its retailers and selling products consumer-direct. This can be done either though Click & Collect Programs (relegating retailers to being fulfillment centers with huge inventory investments) or through company-owned stores ("vertical market integration"). Again, this is happening, but net gains for suppliers are modest at best.

- It can win market share from its competitors. This is notoriously difficult when there are a large number of competing brands with products more or less at parity and no strong brand differentiation, and even more so in enthusiast (which is to say, low-margin) categories, where there's less money to spend on differentiating in the first place.

Frankly, none of these things are likely to happen without invoking the alter the company's long-run profitability element of the equation. Which suggests that both the Quadrumvirate and Shimano are now at optimal market share. And likely to remain there for the foreseeable future.

Fifteen years since its onset in the mid-2000s, Bike 3.0 finds itself in a dilemma. The model's strategy was predicated on the collapse of both retailers and competitive brands. Instead, with the exception of Shimano, no player has accrued enough market share to trigger the prophesied 3.0 eschaton.

The market is stable enough now ... for the top players. But it's a chaotic and dystopian existence for everyone else. I also suspect there is a significant amount of churn as new suppliers and retailers appear and disappear, although there are no reliable numbers available to document this.

So what next? To paraphrase author Joseph Heller, things right now are about as good as they can possibly be ... without getting a whole lot worse than they already are.

Unfortunately, they're about to get a whole lot worse. But that's a topic for another time.